In the wake of the COVID-19 pandemic, businesses around the globe were forced to navigate unprecedented economic challenges. The UK government introduced a lifeline to help small and medium-sized enterprises (SMEs) survive the economic downturn—the Bounce Back Loan Scheme (BBLS). This initiative provided quick and accessible financial support to struggling businesses, offering favorable loan terms to keep them afloat during the crisis.

What is a Bounce Back Loan?

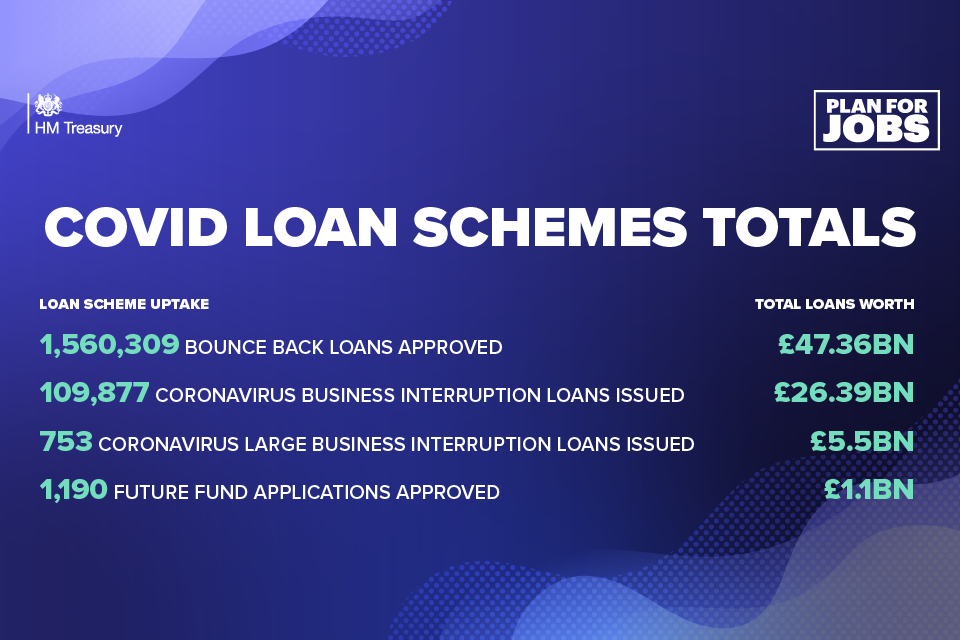

A bounce-back loan is a government-backed financial aid scheme designed specifically to support UK-based businesses affected by the pandemic. The program, launched in May 2020, was part of a broader range of financial relief initiatives aimed at mitigating the economic impact of COVID-19. The scheme offered businesses loans ranging from £2,000 to £50,000, up to a maximum of 25% of their turnover.

One of the most attractive features of a bounce-back loan is the favorable terms. The loans were provided at an interest rate of just 2.5% per annum, with the government covering the interest payments for the first 12 months. Additionally, businesses had the flexibility to repay the loan over up to six years, with no early repayment penalties.

How the Bounce Back Loan Worked

For businesses in need of immediate financial relief, the bounce-back loan application process was straightforward and designed to be quick. The application could be completed online, and funds were often received within a matter of days. This accessibility made it an essential tool for businesses struggling to pay for operational costs such as rent, wages, or inventory.

Unlike traditional loans, businesses applying for bounce-back loans were not subjected to credit checks or intensive scrutiny. This leniency aimed to expedite the process and provide rapid relief to as many businesses as possible. The government also assured lenders that they would cover 100% of the loan in the event of default, which gave banks the confidence to issue these loans without hesitation.

Eligibility Criteria for a Bounce Back Loan

The bounce-back loan was not available to every business, but the eligibility criteria were designed to be broad to include the majority of SMEs. Here are the key criteria that businesses had to meet:

- UK-based business: The business had to be operating within the UK and must have been established before March 1, 2020.

- Adversely affected by COVID-19: The business needed to show that it had suffered a negative impact as a result of the pandemic.

- No previous state aid breaches: The business could not be in bankruptcy, liquidation, or undergoing any form of debt restructuring at the time of the application.

- No existing BBL or CLBILS loan: Businesses that had already received a loan under the Bounce Back Loan Scheme or the Coronavirus Business Interruption Loan Scheme (CBILS) were not eligible to apply for another loan.

Benefits of a Bounce Back Loan

The bounce-back loan scheme provided several advantages that made it a vital part of business recovery during the pandemic. Key benefits included:

- Speed of access: Businesses could receive funds within days, which was crucial for maintaining operations during periods of lockdown.

- Low-interest rate: The fixed 2.5% interest rate was significantly lower than most commercial loans, making repayment manageable.

- No payments in the first 12 months: With the government covering the first year of interest, businesses could delay repayments until they were more financially stable.

- Repayment flexibility: Repayment terms of up to six years allow businesses to spread out the financial burden over time. Moreover, businesses could pay off the loan early without facing penalties.

Challenges and Criticisms of the Bounce Back Loan

While the bounce-back loan scheme was widely praised for providing essential financial support, it was not without its challenges. One of the major concerns raised was the potential for fraud. Due to the ease of the application process and lack of rigorous checks, some businesses misrepresented their financial status to receive larger loans than they were entitled to.

According to reports, there were also instances where loans were taken out by fraudulent entities or individuals with no intention of repayment. The UK National Audit Office estimated that between £3.5 billion and £6.3 billion of the £47 billion lent under the scheme could be lost to fraud.

Additionally, some businesses struggled with the repayment schedule once the 12-month interest-free period ended. While the government introduced a “Pay As You Grow” scheme to extend the repayment period and reduce monthly payments, the ongoing economic challenges caused by the pandemic meant that some businesses still faced difficulties repaying the loans.

The Impact of Bounce Back Loans on Businesses

For many businesses, the bounce-back loan scheme was nothing short of a lifeline. It enabled companies to continue operating during the most challenging periods of the pandemic when revenues plummeted due to government-imposed restrictions.

The funds were often used to cover essential expenses such as rent, salaries, and supplier payments, helping to maintain operations while businesses adjusted to the new economic reality. For businesses in industries such as hospitality, retail, and travel, which were disproportionately affected by lockdowns, the bounce-back loan offered a critical buffer until the economy began to recover.

In some cases, businesses even used the loan to invest in new strategies, such as digital transformation, that allowed them to pivot to online sales or services, opening new revenue streams.

Pay As You Grow and Loan Repayment Options

Recognizing the ongoing difficulties faced by businesses, the UK government introduced the Pay As You Grow (PAYG) scheme in 2021 to provide greater flexibility in repaying bounce-back loans. Under this scheme, businesses were given three main options:

- Extend the loan term: Businesses could extend their loan period from six years to 10 years, reducing the monthly payments.

- Interest-only payments: Businesses could choose to make interest-only payments for six months, a measure that could be used up to three times during the loan term.

- Payment holiday: Businesses could take a six-month payment holiday, pausing both interest and principal payments for six months.

These measures were intended to ease the burden on businesses that were still struggling to recover from the economic impact of the pandemic, providing additional breathing room for repayment.

Conclusion: The Legacy of Bounce Back Loans

The bounce-back loan scheme played a crucial role in stabilizing the UK economy during one of the most challenging periods in recent history. While not without its challenges, the scheme provided fast and accessible financial relief to thousands of businesses, allowing them to navigate the difficulties of the pandemic.

As the economy continues to recover, the legacy of the bounce-back loan will likely be seen in how it allowed businesses to maintain their operations and even innovate in response to a rapidly changing world. For those businesses that successfully repaid their loans, the bounce-back loan served as a lifeline that helped them “bounce back” from the brink of financial collapse.

{kind=link}